Bet Live and In-Play at Offshore Books with Eyes Open on the Feed Lag

Live odds at offshore books are produced by a feed plus model plus trader stack; understanding the stack tells you where the operator is fast and where the operator is slow.

Feed lag was the original edge; the marquee markets have closed the gap, but micro markets and second tier sports remain exploitable for disciplined bettors.

Cash-out is structurally negative expected value because the bettor pays a second margin on the remaining outcome; tactical exceptions exist on correlated parlays.

Same game live parlays compound margin geometrically; the rare exceptions are operator pricing bugs on correlated legs that get patched within weeks.

Live UX varies sharply across operator families; the rotation of choice for live betting includes a Pinnacle school book, an Asian style book, and a mass market book for product breadth.

In-play betting is where the offshore product visibly outpaces regulated apps; the price comes from a feed, a model, and a trader, and every link in that chain has a lag profile.

Why offshore live betting is the most differentiated part of the product

Live in-play betting is the single market category where the offshore sportsbook product visibly outpaces the regulated domestic apps. Every drive, every set, every over, every change of possession turns into a bet. The market depth is extreme: a typical major offshore book runs forty to ninety live markets on a top tier event in the closing minutes, where a regulated app might run ten or fifteen. The product breadth is the marketing surface; the operational reality of betting that breadth is where the edge and the trap diverge.

The bettor needs three things to operate seriously in live: a working mental model of how the operator priced the market, a low latency stream of the actual event, and a placement workflow fast enough to act inside the operator’s acceptance window. The first is the analytical work; the second is an infrastructure decision; the third is operational discipline. The bettor that has all three runs at materially better expected value per bet than the bettor that has only the bet menu in front of them and a delayed broadcast in the background. Live volume is also where the limit hygiene from the high limit page earns its keep; live bet sizing on a sharp tolerant operator outpaces the same bet sizing on a mass market book inside a single session.

The product side of the offshore sportsbook stack is treated on the offshore sportsbooks pillar in detail. This page covers the live specific layer above that: how live odds are made, where lag arbitrage actually pays, what micro markets are worth running, the cash-out trap, and how the major operator families compare on live behaviour. The objective is operational: by the end of the page the bettor knows which of the operators in their rotation to bet which live markets at, and which markets to skip entirely.

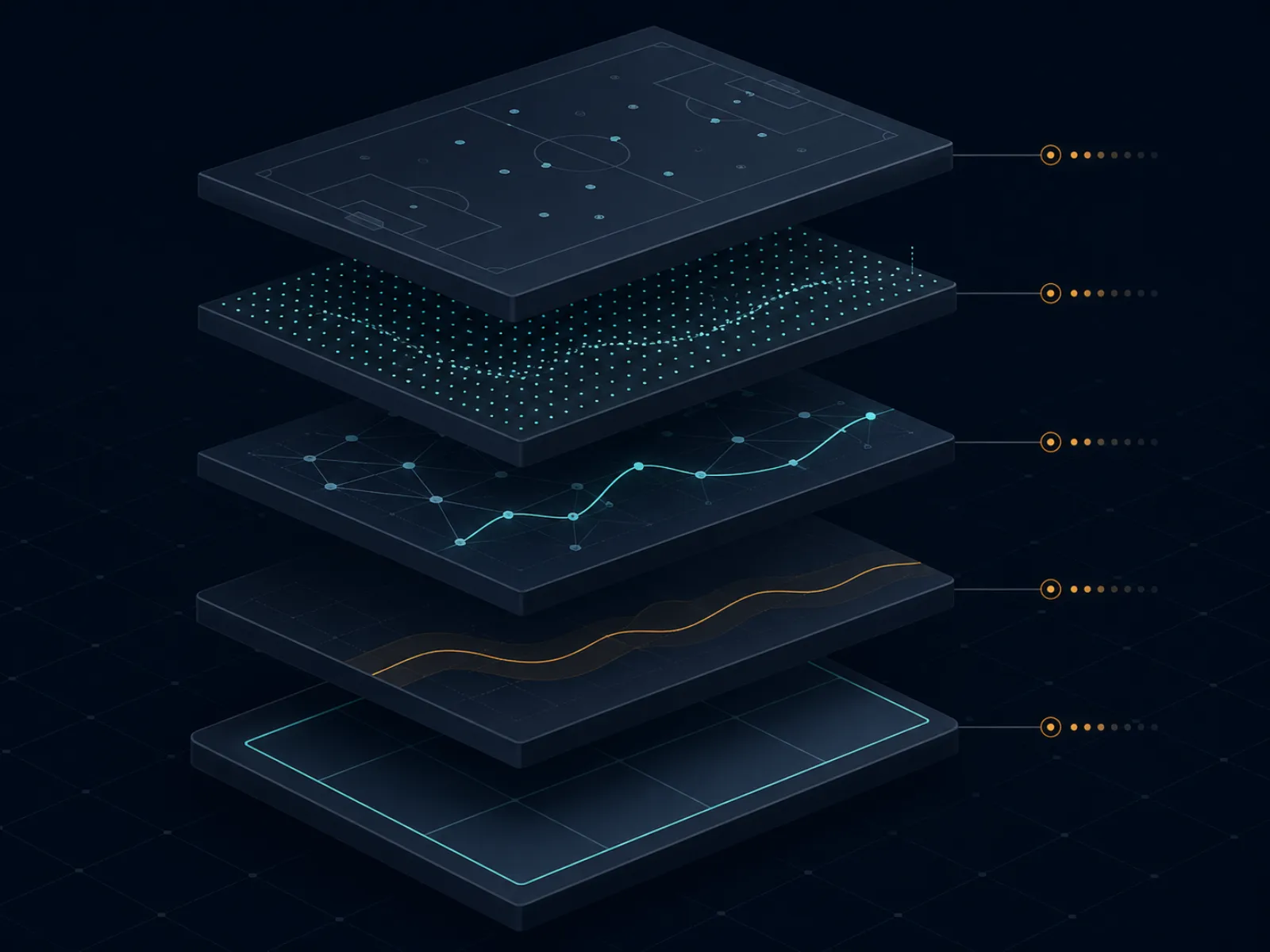

Concept primer: how a live price is made

The illustration below shows the live odds production stack at a major offshore book. Five layers run sequentially from on field event to bettor screen, and each layer has a lag profile that shapes the operator’s price relative to the true probability of the next outcome.

The live odds stack: on field event, data feed, in-play model, trader markup, bettor screen. Each layer adds its own lag and its own margin.

Layer one is the data feed. A data vendor (Sportradar, Genius Sports, Stats Perform are the dominant names) collects the on field event data through a combination of in-stadium scouts, broadcast feed scrapers, and official league data partnerships. The feed produces structured event objects (a goal, a yellow card, a fault, a wicket, a possession change) within a window of half a second to several seconds depending on the sport and the data partnership. The lag from on field to feed is the first lag layer.

Layer two is the in-play pricing model. The operator’s trading desk runs a model (proprietary or licensed from a B2B live trading vendor) that converts the structured event stream into updated probabilities for every market on the book. The model latency from feed event to updated probability is in the sub second range for marquee markets and in the few seconds range for niche markets. The model output is the operator’s belief about the price; it is not the price the bettor sees.

Layer three is the trader markup. The model output is a fair probability; the trader desk applies a margin (typically 4 to 8 percent across the live book, varying by sport and by operator family) and decides whether to accept the model output, override it on specific markets, or suspend the markets entirely if the model output disagrees with the model’s confidence interval. The trader behaviour is the operator’s editorial control over the model; on Pinnacle school operators the trader role is light and the model dominates, while on mass market operators the trader role is heavier and the prices are more managed.

Layer four is the price publication and acceptance window. The new price is published to the bettor screen, the operator opens an acceptance window for bets at that price, and bets placed in the window are accepted if the operator’s risk model approves the specific bet. The acceptance window can be milliseconds (during fast moving moments) or seconds (during steady state). Layer five is the bettor screen and broadcast lag, which is everything from the bettor’s ISP to the broadcaster’s delay; it is outside the operator’s control but inside the bettor’s decision loop.

Worked example one: the lag arbitrage gap on a tennis service game

Tennis match in progress, top tier event. Server holds three break points against on the current game. The operator’s in-play model converts a saved break point into a small but immediate revaluation toward the server. The chain of lags: data feed publishes the saved break point at T+1 second, model updates the game winner price at T+1.4 seconds, trader markup applies and price publishes to bettor screen at T+2 seconds. The bettor on a live stream with one second latency sees the saved break point at T+1 second; the bettor watching a broadcast with twenty second latency sees the moment at T+20 seconds.

The gap that the operator is open to lag arbitrage is the second from T+1 to T+2 seconds, during which the on stream bettor knows the price will move but the operator has not yet moved it. A bet placed at T+1.5 seconds by a low latency bettor at the pre move price is the lag arb. The bet size that crosses without rejection is the binding constraint; major operators run automated lag detection that suspends the market the moment the model and the published price diverge by more than a small threshold, so the lag arb window in practice closes inside half a second on marquee markets.

The numbers, assuming a representative tennis market on a top operator. Pre save break point game winner price: server at decimal 1.95, returner at decimal 1.85. Post save price (after model and trader): server at decimal 1.55, returner at decimal 2.45. The pre move price implies a server probability of 51.3 percent; the post move price implies 64.5 percent. A bet of 1,000 USD on the server placed at the pre move price returns 1,950 if the server holds. The fair value of the position at the post move probability is 1,000 * 1.95 / 1.55 = 1,258 USD. The lag arb captured 258 USD of structural value on a 1,000 USD bet, a 25.8 percent edge per trade.

The operational reality. The operators that the lag arb still works against are the smaller offshore books with looser suspension behaviour and slower model updates. The Pinnacle school operators have closed the gap on tennis service game markets through aggressive suspension and lower margins; the lag arb is detected and the bet is voided under "obvious error" or the market is suspended before the bet places. The bettor that wants to run lag arb in tennis service games operates at second tier offshore operators where the trade still works, accepting a higher void risk on detection in exchange for a window that has not closed.

Worked example two: cash-out math on a partially won parlay

Three leg pre game parlay placed at offshore book A. Leg one: home side at decimal 1.91 (a 47.6 percent implied). Leg two: total over at decimal 1.95 (51.3 percent). Leg three: alternate spread at decimal 2.10 (47.6 percent). Combined parlay decimal: 1.91 * 1.95 * 2.10 = 7.82, with an implied probability of 12.79 percent and a stake of 100 USD that returns 782 USD if all three legs hit.

Mid game, leg one and leg two have settled positively; the home side won and the total went over in the third quarter. Leg three is still open: alternate spread on a basketball game where the favourite leads by 9 points heading into the final period and the alternate spread is favourite -8.5. The operator offers a cash-out price of 360 USD on the open position. The bettor must decide: take the 360 USD locked, or hold the bet for the 782 USD payout if leg three lands.

The fair value calculation. The remaining bet is now a single leg at decimal 2.10, paying 782 USD on a 100 USD stake (the parlay-equivalent stake of the open leg). The fair value is the implied probability that the favourite covers -8.5 from a 9 point lead with one quarter remaining. A simple in-play model on basketball spreads in this configuration produces a covering probability around 55 percent (the lead is enough that the cover is a fairly-priced toss-up with some advantage to the favourite). The fair value of the open position is 0.55 * 782 = 430 USD. The operator’s 360 USD cash-out offer is 16 percent below fair value; the cash-out is -EV by 70 USD on this single decision.

The tactical exception. If the bettor has new information the operator’s pricing has not yet absorbed (the leading team has just lost a star player to fouls, the trailing team is shooting hot from beyond the arc, the official line has tightened the game in a way the cash-out price does not yet reflect), the cash-out can become +EV. The discipline is to treat the cash-out as a trade decision with its own analysis, not as a default exit. The default behaviour for a disciplined bettor is to decline cash-out and let the variance run; the cumulative EV of declining cash-out across hundreds of partially settled parlays is a measurable positive return that is mostly hidden because the variance is high on any single decision.

Micro markets that pay and the ones that look like they pay

Micro markets are the in-game markets that resolve in minutes rather than over the full event. Tennis service game winners, basketball quarter winners, soccer next goal, cricket next over runs, gridiron football next drive outcome. The market category is dense at offshore books and creates the impression that every micro market has edge; in practice only a small subset is worth playing for a non specialist bettor.

The micro markets that pay share a structural property: the operator’s pricing model is slow on the relevant signal relative to a focused bettor’s knowledge. Tennis service game winners are slow because the model under weights momentum signals (the bettor watching the match knows the server has been holding comfortably and the operator’s model is still pricing on tour level baseline). Cricket session totals are slow because the operator’s model under weights pitch deterioration and on field tactical adjustments. Basketball quarter totals are slow because the recreational bettor pool on quarter totals is small and the operator’s margin is competitive but the model has less data to refine the price.

The micro markets that look like they pay but do not include same game live parlays on independent legs (the operator prices correlation correctly more often than not), next goal on soccer with no model data refresh from the in-play feed (the price is just the implied half time line shifted by elapsed time), and basketball next basket markets (the operator has tight margins that compress the bettor’s edge to near zero). These markets can be marketing flags that pull the recreational bettor in, with implied margins higher than the marquee market on the same event.

Operationally, the disciplined micro market workflow runs only two or three sport categories at any one time, paired with the bettor’s actual sport knowledge depth. Combat sports live betting between rounds is one of the cleanest sport specific edges on offshore live menus and is treated separately on the combat sports page; the major North American sports calendar of edge windows is on the major leagues page. The bettor that knows tennis runs tennis service game and set winner micro markets; the bettor that knows cricket runs session totals and over by over markets; the bettor that knows basketball runs quarter totals and pace based markets. The bettor that runs every sport thinly is paying margin without the analytical depth to convert it.

The rare tactic: pre-suspension flash betting on broadcast trigger events

Most live betting literature treats market suspension as a wall the bettor cannot cross. There is a window before suspension where the bettor with the right setup can place bets at pre move prices on flash events the operator’s model has not yet absorbed. The window is small (typically under two seconds) and only opens on specific event categories, but the cumulative edge across a season is structural for a bettor who runs the workflow.

The relevant event categories. In tennis: the moment a player calls the trainer, the moment a serve clock violation is announced, the moment a challenge succeeds. In soccer: the moment the referee shows yellow but before the booking is processed by the data feed, the moment a substitution is signalled at the fourth official board. In gridiron football: the moment a video review is initiated, the moment a key player limps off after a play. In each case the broadcast announces or visually shows the event seconds before the data feed publishes a structured event object the operator’s model can act on.

The workflow is mechanical. The bettor watches the low latency stream with a finger on the bet placement button. When the trigger event occurs visually, the bettor places the bet at the existing price before the data feed updates. The operator publishes the new price within a second; if the bettor placed in the window, the bet is accepted at the pre move price. The lag arb bettor profits from the gap between visual event and data feed event.

The tactic is not without risk. Operators that detect the pattern (a bettor consistently placing bets in the half second before suspensions) flag the account for review, sometimes voiding the relevant bets under "abuse of in-play markets" clauses. The mitigation is to run the tactic at moderate frequency only, on markets where the operator’s detection model is least active (cricket and tennis service games are the empirical sweet spots; major North American sports are heavily monitored). The bettor that runs this on every flash event will be flagged within weeks; the bettor that runs it selectively over months extracts the edge without triggering the clause.

Pitfalls: the failure modes that turn live betting into a leak

Trading the broadcast lag instead of the feed lag. The bettor watching a thirty second delayed broadcast and placing bets at "current" prices on the operator’s screen is structurally late on every market. The operator’s price reflects the on field event the bettor has not yet seen; the bet is placed at a post move price the bettor mistakes for a pre move price. The leak is invisible to the bettor because the bet feels normal; only after settlement does the cumulative loss show up. The fix is mechanical: invest in a low latency stream at parity with the operator’s data feed before placing any live bet.

Sizing live bets like pre game bets. Pre game bet sizing is built around an analytical edge the bettor can quantify before the event. Live bet sizing has to account for feed lag risk, suspension risk, partial fill risk, and the higher margin embedded in live prices relative to pre game on the same market (the pre game margin baseline is documented on the line shopping page). Most disciplined bettors run live stakes at half to two thirds of pre game stakes on the same operator for the same event; a bettor that sizes live identical to pre game is overstaking by 30 to 50 percent on the same expected value.

Cash-out by reflex rather than by analysis. The cash-out button is the most psychologically loaded interface on a live sportsbook. It offers immediate variance reduction in exchange for a margin payment that the bettor often does not consciously price. The disciplined behaviour is to treat the cash-out as a separate trade decision with its own fair value calculation; a bettor that takes cash-out reflexively on every partially settled parlay leaks 8 to 15 percent of pre cash-out expected value across the season.

Same game live parlay accumulator drift. Same game live parlays are heavily promoted at mass market offshore books because the geometric margin compounding makes them the highest hold product on the live menu. The recreational bettor builds three to seven leg same game live parlays on whatever feels exciting in the moment; the cumulative margin is in the high teens and the realised return is materially negative across any meaningful sample. The disciplined position is to skip same game live parlays unless a specific correlation pricing bug at the operator creates a defensible +EV trade documented on the arbitrage and +EV page.

Latency stack misconfiguration. Bettors that run a low latency stream alongside the operator’s app sometimes underestimate the latency in the placement workflow itself: app rendering, bet slip confirmation, two factor authentication on each placement, network jitter on a phone hotspot. The compound latency from event to placed bet can exceed the visible stream latency by several seconds; the bettor thinks they are early on the feed and is in fact late. Audit the placement workflow end to end and time it on a representative event before relying on the latency advantage.

Operator suspension as a free option for the operator. Some operators suspend markets aggressively during normal play and reopen with a wider margin. The bettor placed at the pre suspension price thinks they have the edge; the operator reopens with a price that often invalidates the original price under "obvious error" clauses, voiding the bet retroactively. The mitigation is to know the operator’s suspension posture before relying on pre suspension placements; the safety page covers the void clauses to grep for in the T&C.

In-play scoring errors. The data feed occasionally errors (a goal incorrectly attributed, a wicket reversed by a third umpire decision the feed misclassifies). The operator settles bets on the feed; corrections happen but slowly. The bettor that places live bets on the moment of a feed event is carrying feed reliability risk; over a year a small fraction of bets settle incorrectly and require manual escalation. Build the operational discipline to log every live bet with timestamp and screenshot for any disputed settlement, and accept that a single percent of in-play bets will need post settlement work.

Frequently asked questions

How big is feed lag at offshore live books in practice?

Feed lag from on field event to operator price update sits in a window of three to fifteen seconds at major offshore books, with crypto first books often at the slower end and Pinnacle school operators at the faster end. The bettor watching a delayed broadcast (typically an additional five to thirty seconds behind the feed) is structurally late on the operator’s price; the bettor watching a low latency stream is structurally early. The arbitrage that lives in this gap was the original edge in live betting; the major operators have closed it on marquee markets through suspension behaviour but it remains real on niche markets.

Is cash-out ever a +EV decision?

Almost never on a single bet basis, occasionally on a portfolio basis. The cash-out price is the operator’s current implied price for the remaining outcome plus a margin (typically 4 to 8 percent) on top of the original bet’s margin; the bettor is paying juice twice in exchange for variance reduction. The exceptions are tactical: cashing out a leg of a multi leg parlay where one leg has hit and the remaining legs are correlated against the position, or cashing out when the bettor has new information the operator does not yet reflect in the cash-out price. As a default behaviour, declining cash-out on every offer is the disciplined position.

What is a micro market and which ones are worth playing?

A micro market is an in-game market with a defined short term resolution: next drive in gridiron football, next point in tennis, next over in cricket, race to a target score, next set winner. The markets resolve in minutes rather than over the full event, which lets the bettor cycle decisions quickly. The worth playing list depends on the operator and the sport. The empirically valuable micro markets at offshore books are tennis service game winners (the operator pricing is often slow to react to a break point flash), cricket session totals (where the live model lags the on field momentum), and basketball quarter totals (where the operator margin is lower than full game totals because the recreational bettor pool is smaller). The traps include same game live parlays where the legs are heavily correlated and priced as if independent, but in the wrong direction.

How do offshore books handle market suspension during a key moment?

Differently by operator family. The Pinnacle school books suspend immediately on uncertainty (penalty awarded, video review pending, injury timeout), reopen with a new price within seconds, and accept bets at the new price. The mass market offshore books suspend longer, often through a cluster of related markets, and reopen with a wider margin. The crypto first books vary widely; some suspend aggressively to protect against feed scraping, others run loose and absorb the lag risk through margin. Knowing the suspension posture of each operator in the rotation is operational work; the bettor that runs only on the operator family with the suspension behaviour they understand has a structural advantage on the placement timing.

Are live parlays a viable strategy or always a juice trap?

Mostly the latter, with narrow exceptions. The live parlay product at offshore books takes the existing margin on each individual leg and multiplies it geometrically; a three leg live parlay at -110 per leg has an effective margin in the high teens once correlation is priced in. The exceptions are correlated parlays where the operator has not adjusted for correlation: same game live parlays on totals plus alternate spreads where one leg implies the other in a direction the operator’s pricing model treats as independent. These are operator specific bugs that come and go; they are real edge while they last and the operator usually closes the gap within a few weeks of detection.

How does live betting compare across operator types?

The live UX axis is real and underrated. Pinnacle school operators offer fewer markets but tighter prices and faster bet acceptance; the live trader desk leads on price accuracy. Asian style operators offer the deepest live Asian handicap markets in soccer at the lowest margins, with very fast suspension behaviour. Mass market offshore books offer the broadest live market menu, including same game live parlays and proposition heavy build out, at the cost of higher margin and slower price update. Crypto first books are uneven; some have built strong live platforms (often white-labelled from a B2B live trading provider) while others bolt live on as a thin add on. The page on the offshore sportsbooks pillar covers the product side context for these differences.

We use necessary cookies to make this site work. We would also like to set optional analytics cookies to understand how visitors use the site. You can change your choice at any time from the footer.