Run Arbitrage and +EV at Offshore Books Without Burning the Account

Sustainable offshore arbitrage ROI is one to four percent of turnover before voids and fees, not the eight to twelve percent that screen-scrape tools advertise on transient lines.

+EV betting is the longer game; it survives operator scrutiny better than arbitrage because the bet pattern matches a sharp recreational profile rather than a paired hedge.

Offshore book tolerance for arb varies wildly; the same operator family can flip posture mid season as the trading desk leadership rotates.

Bonus arbitrage is the highest ROI per hour but carries the highest void risk; isolate the bonus account from the +EV and pure arb stack so a void does not cascade.

Tool coverage of offshore books is partial; the largest spreads live on Asian style and crypto first books that most odds aggregators index incompletely.

Arbitrage at offshore books is cat and mouse; +EV is the longer game; both survive only with discipline on the void clauses.

What arbitrage and +EV actually are, in one section

Arbitrage at sportsbooks is the practice of placing two or more bets across operators on the opposite outcomes of the same event such that the sum of the implied probabilities is below one hundred percent; the spread between the implied total and one hundred percent is the locked return on the trade, irrespective of the actual outcome. The mechanics are arithmetic: if operator A prices the home side at decimal 2.10 and operator B prices the away side at decimal 2.05, the implied probabilities sum to 47.62 + 48.78 = 96.40 percent, leaving a 3.60 percent margin that is the arb return on stake distributed across the two sides in inverse proportion to the prices.

+EV betting is the practice of placing a single sided bet at a price that beats the market consensus close (the price the market converges to a few minutes before kickoff or tip off, which is the cleanest published estimate of the true probability). A +EV bettor does not lock the return; the bettor accepts the variance of the actual outcome and relies on the law of large numbers to convert positive expected value per bet into positive realised return over hundreds of bets. The closing line value (CLV) signal is the proxy: an account with a sustained 3 cents per bet positive CLV across a sample of two hundred bets is operating at roughly 3 percent ROI before juice, before voids, and before operator counter measures.

The two strategies are commercial cousins. Arbitrage requires more operators, more capital, more rebalancing, and lives or dies on operator tolerance for paired bets. +EV requires fewer operators (a sharp tolerant book and a reduced juice book are enough as covered on the high limit page and the line shopping page), more model work upstream of the bet, and survives operator scrutiny more easily because the bet pattern is single sided. Bettors operating at scale usually run both, on segregated accounts so a void on the arb side does not contaminate the +EV side.

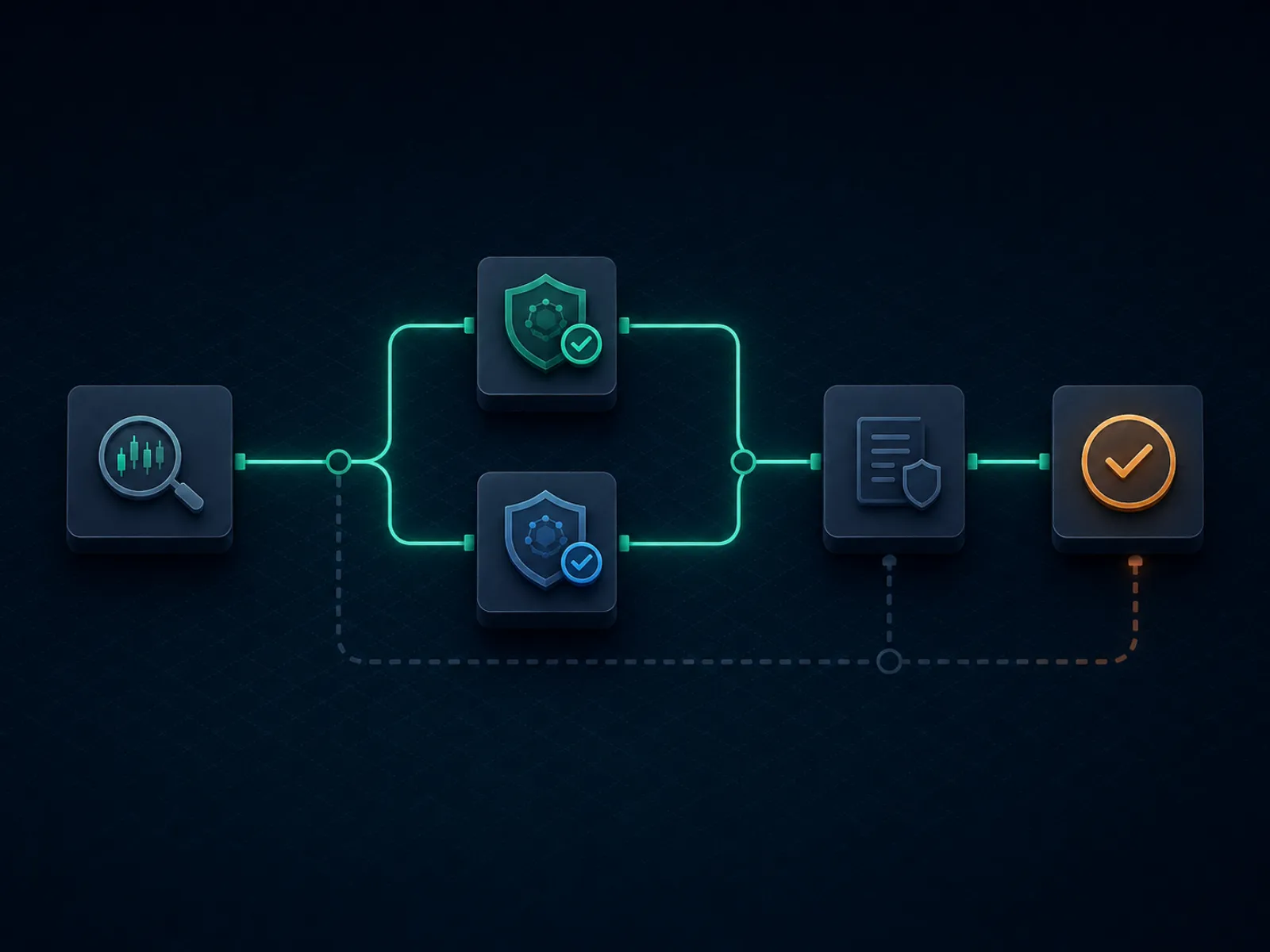

Concept primer: how an arb is structured end to end

The illustration below maps the operational flow of a single offshore arb from tool detection to settlement. Each step is a real choke point where the trade can fail; the discipline is to know which choke point fails most often on the operator pair you use and to size the trade so the failure is survivable.

A clean arb survives every step; a contaminated arb fails on the void clause, not on the math.

The flow has eight steps in production. Tool detection of a candidate arb is step one; the tool publishes a spread and the prices it expects at each operator. Manual price verification at both operators is step two and the most often skipped; the published price is stale by the time the tool surfaces it, and the actual price at the cashier is often a few cents different from the tool price. Stake calculation is step three, derived from the verified prices and the available bankroll at each operator. Sequential placement is step four; place the side that is most likely to move first (typically the side at the smaller operator with thinner liquidity), then the second side at the larger operator. Confirmation that both bets are accepted at the calculated prices is step five.

Settlement is step six and the first place void clauses come into play; the operator may settle one side, then re grade the other side under an "obvious error" or "palpable error" clause if the line was off market. Withdrawal is step seven and the second place voids come into play; an arb identified by the operator’s post settlement risk team can be voided after withdrawal request, with the operator returning the original stake but seizing any associated bonus. Rebalancing the float across operators is step eight, on a weekly cycle, settling the loop so the next arb does not have to wait on a deposit hop.

Worked example one: a clean two way arb on tennis

Marquee tennis match, the favourite priced at decimal 1.55 at a crypto first operator (the Asian style operator is closing in on it but not quite there yet). The dog priced at decimal 2.85 at a Pinnacle school operator. Implied probabilities: 64.52 percent on the favourite, 35.09 percent on the dog, total 99.61 percent. The arb spread is 0.39 percent, which is below the threshold most arb tools publish; this trade is on the boundary and would be marginal at most operators because of the void risk and the rebalancing cost.

For the worked numbers, assume a ten thousand USD aggregate stake. Stake on the favourite at 1.55: (10,000 / 1.55) / (1/1.55 + 1/2.85) = 6,452 / 1.0009 = 6,446 USD; the bet returns 6,446 * 1.55 = 9,991 USD if it wins. Stake on the dog at 2.85: 10,000 - 6,446 = 3,554 USD; the bet returns 3,554 * 2.85 = 10,128 USD if it wins. Locked return: between 9,991 and 10,128 USD on a 10,000 USD outlay, a 0.91 to 1.28 percent return per arb. The headline 0.39 percent spread becomes a 0.91 percent return at the lower side because the unequal stake distribution overweights the longer odds slightly to balance the payouts.

Now the realistic adjustments. The favourite price drifts from 1.55 to 1.53 during the placement window, eroding 0.4 percent of the spread before the trade locks. The dog operator applies a 1 percent withdrawal fee on the cashier when the bettor cycles funds; that is another 0.4 percent of working capital per arb across the full trade size. Net of the two adjustments, the locked return falls to roughly 0.1 to 0.5 percent on stake, and a single voided bet across a sample of one hundred trades wipes out the cumulative return. The trade is structurally marginal; an arber would skip it and wait for spreads above 1.5 percent. The pedagogical lesson is that the arithmetic spread is not the trade ROI; the realised ROI is net of price drift, fees, voids, and rebalancing drag, all of which compress the headline number.

Worked example two: bonus arbitrage on a deposit match

Offshore book offers a 100 percent deposit match up to 1,000 USD, with a 10x rollover requirement on deposit plus bonus, contribution rates of 100 percent on sides and totals at minimum odds of decimal 1.50, and a maximum cashout of 5x the bonus. The effective rollover is (1,000 + 1,000) * 10 = 20,000 USD of qualifying turnover before the bonus and any associated winnings can be withdrawn. The bonus arb is the practice of clearing this rollover at minimum theoretical loss while hedging at a second operator to dampen variance.

The math, assuming a -110 (decimal 1.91) market structure. Expected turnover loss on each qualifying bet: 1 / 1.91 = 52.36 percent implied probability versus a fair 50 percent (assuming the line is roughly fair), so the per bet expected loss is 100 stake * (50% * 1.91 + 50% * 0 - 100) = -4.5 USD per 100 staked. Across 20,000 USD of turnover, expected loss is 20,000 * 4.5% = 900 USD. The bonus is 1,000 USD; expected value of clearing the rollover is 1,000 - 900 = 100 USD, or 5 percent of capital committed (deposit) over the rollover cycle. That is the floor, before hedging.

Now the hedging adjustment. By hedging each bet at a second operator on the opposite side, the bettor compresses variance from the binary outcome of each bet to the small spread between the two operators’ prices. The effective per bet cost rises slightly because the hedged price pair is below 100 percent only by the arb spread (typically 0.5 to 1.5 percent). The hedge converts the 900 USD expected loss with high variance into a 1,000 to 1,100 USD expected loss with near zero variance, depending on the average arb spread the hedge captures. Net realised value of the bonus drops from 100 USD pre hedge to roughly minus 100 USD post hedge if you hedge at exactly fair; the bonus arb is profitable only if you hedge at operators where you also collect a small arb spread on each leg.

The operational realisation. A pure deposit match bonus is rarely worth hedging fully; the better approach is partial hedging on the largest individual bets only, accepting variance on the small bets. The realised value of the bonus moves to roughly 200 to 400 USD depending on rollover discipline and on which operator pair the hedging side runs at. Across a portfolio of bonuses (the welcome bonus at five operators across a quarter), the total realised value is in the 1,000 to 2,000 USD range on 5,000 USD of deposits, a 20 to 40 percent gross return on capital before voids and clawbacks. The pitfall section below covers what happens when the bonus arb gets voided.

Tool coverage and the operators the tools miss

The arbing toolset that recreational and semi pro arbers use is small and well known. The leading vendors index thousands of markets across hundreds of operators in real time, surfacing arbs the moment the implied probabilities cross below one hundred percent. The vendors charge subscriptions in the hundreds of USD per month and publish tutorial content that markets the work as turnkey. The product is real; the limits of the product are commercial.

The first limit is operator coverage. The tools index the largest operator families because the integration cost per operator is high and the marginal arb supply per smaller operator is low. The Asian style operators that run handicap heavy soccer markets, the crypto first operators that run thin lines on niche sports, the regional operators that publish odds in local language interfaces, are all under indexed. The result is structural: the largest arb spreads live precisely on the operators the tools miss, because the tool surfaced arbs at major operators are competed away to near zero by the population of subscribers placing the same bets at the same time.

The second limit is detection. The operators that the tools do cover see the bet pattern of tool footprint accounts (a cluster of accounts placing the same arb within minutes of each other on the same niche market) and apply void clauses to the entire cluster. The detection is not magical; the operator simply sorts the bet log by market and timestamp and the cluster is visible by inspection. Tool subscribers operating without disguise (placing every flagged arb, sizing identically across accounts, settling on identical cashier rails) become identifiable to the operator within weeks.

The serious arber operates the tools as a watch list rather than a placement queue. The tool surfaces a candidate; the arber verifies the price manually at both operators, sizes the trade based on actual cashier behaviour rather than tool defaults, and skips the trade if the arb is in the cluster zone the operator already monitors. The remaining trades are fewer in number but materially safer; the operational ROI net of voids ends up higher than an unfiltered tool subscriber sees.

The rare tactic: middle bets on totals as a +EV per arb hybrid

Most arbing literature treats arbitrage and +EV as separate strategies. There is a hybrid trade that sits between them and that the SEO ranking content rarely covers properly: the middle bet on totals markets, where the bettor places the over at one operator at a number, the under at a second operator at a higher number, and wins both bets if the actual total lands inside the gap. The trade has the bet structure of an arb (two operators, opposite sides) but the payoff structure of a positive EV trade (the gap creates a region of double payoff with negative cost on either single leg).

A worked example. Basketball total at operator A: over 215.5 priced at decimal 1.95. Basketball total at operator B: under 217.5 priced at decimal 1.95. Stake 1,000 USD on each side, total outlay 2,000 USD. Outcomes: total below 215.5, lose at A, win at B, return 1,950, net minus 50; total above 217.5, win at A, lose at B, return 1,950, net minus 50; total exactly 216 or 217, win at A, win at B, return 3,900, net plus 1,900. The trade locks a 50 USD loss outside the middle and a 1,900 USD win inside the middle; it is +EV if the implied probability of the total landing in 216 or 217 exceeds 50 / 1,950 = 2.56 percent.

The relevant probabilities in production NBA totals are typically 4 to 8 percent for a two integer middle, depending on the line and the team pair, putting the trade firmly in +EV territory. The middle bet survives operator scrutiny better than a pure arb because the bet pattern at each operator is single sided and the operator does not see the paired position; the middle exists only in the bettor’s aggregate book, not in the operator’s view. The trade is harder to source than a pure arb because it requires a real line gap (not a price gap) at the same moment between two operators on the same market.

The hybrid runs cleanly on the major North American verticals and on top European soccer totals. It does not run on Asian handicap markets because the line gaps are too small. It is most fruitful in the hour before kickoff or tip off when soft books are slow to follow market wide moves and the gap opens to two integers or more. Disciplined middle hunting across one hundred trades per quarter produces a return profile in the 4 to 8 percent range on capital deployed; that is structurally above the pure arb ROI net of voids, with materially lower operator detection risk.

Pitfalls: the failure modes that turn a profitable arb book into a loss

The "irregular play" or "low risk betting" T&C clause. Most offshore books carry a clause permitting the operator to void any bet the operator considers irregular, including but not limited to arbitrage, hedging, low risk strategies, and bonus abuse. The clause is broad by design; the operator’s discretion is the binding constraint. Read every operator’s T&C for this clause before depositing; the operators that scope the clause narrowly (specifying that void applies only to bonus interaction) are the operators arbers can use safely. Operators that scope the clause broadly are unusable for arbing regardless of the headline prices.

The "obvious error" or "palpable error" clause. Operators reserve the right to void bets at "obviously incorrect" prices, the definition of which is again operator discretion. The clause sits on top of the arbing trade because the wrong side of an arb (the operator with the better price on the leg) is the operator most likely to invoke palpable error. Disciplined arbers avoid trades where one leg is materially off market relative to closing line; the off market price is exactly the price the operator will void if the bettor wins.

Bonus clawback on void. If a bonus arb is voided, the operator returns the deposit and seizes the bonus. The bettor loses the value of the rollover work already completed and any associated winnings. The rare but real failure mode is the operator clawing back deposit alongside the bonus, citing "fraudulent bonus abuse"; the cashier returns net deposit minus the cleared losses on the bonus side, leaving the bettor materially down on the cycle. The operational mitigation is to separate bonus accounts from the main arb stack, so a clawback hits a small pre committed slice of bankroll rather than the operational float.

Cashier rebalancing drag. Arb capital must be rebalanced across operators after every trade cycle; the rebalance cost is a real ROI drag. Card and wire rails turn rebalancing into a multi day blocker that idles tens of thousands of USD; crypto rails settle in hours but carry on chain fees that compound across the float. The disciplined arb operation runs entirely on stablecoin rails (USDT or USDC on a low fee chain like Tron or Polygon) to compress rebalance time and fees together; the trade off is that the operator pool drops to operators that accept the chosen stablecoin, and the relationship is covered on the payments page.

The post withdrawal void. The operator settles the bet, releases the withdrawal request, processes the cashier, and then voids the bet a week later when the post settlement risk team reviews the account. The funds are clawed back from the next deposit; if the bettor never deposits again, the operator marks the account negative and refers to the shared offshore industry blacklist database. The bettor is not bankrupted but loses access to that operator family permanently. The honest framing: a quarter of the offshore arb book lives under this risk, and the void rate is in the low single digit percent range across a year of placements.

Tax and reporting. Even in jurisdictions where offshore betting is legal at the player level, a high turnover arbing operation generates significant gross betting revenue numbers that may be reportable. The site avoids country specific tax discussion by policy; the operational point is that arb turnover is a different reporting object from arb net income, and bettors should consult locally before scaling the operation. The legality framework page covers the player side reporting questions in jurisdiction neutral terms.

Account concentration. A successful arber accumulates working balances of 5,000 to 30,000 USD per operator across a rotation of six to ten operators. Concentrating more than a quarter of the float at any single operator is a single point of failure on the bankroll axis; an account closure or a multi week withdrawal hold idles a quarter of the bankroll in one stroke. Spread the float, and treat each operator as a counterparty with finite reliability, exactly as the high limit page recommends for sharp tolerant operators.

Frequently asked questions

What ROI is realistic for offshore arbitrage in 2026?

The honest answer for a disciplined arber is one to four percent of turnover before voids, fees, and currency drag. The headline numbers some tools post (six, eight, twelve percent on a single arb) are real for the moment they exist; the moment passes inside seconds, and the bets are usually on niche markets where the operator voids more aggressively. Net of voids and fees, sustainable arb ROI on offshore books trends toward two percent for an operator with average tolerance and toward zero on operators that void aggressively. Plan the bankroll on two percent and treat anything higher as upside, not baseline.

Will an offshore book void my bet for arbitrage?

Some will, some will not, and the same operator can change posture during the year. The relevant clauses are usually titled "irregular play", "low risk betting", "match betting" or "abuse of promotions"; their actual scope is operator discretion. The arbitrage tolerant operators publish their tolerance implicitly through the way they apply these clauses; they let pure arbs settle, but void anything that pairs an arb with a promotional credit, a free bet, or a bonus that has not cleared rollover. The arb intolerant operators void on the first match and seize the bonus alongside it. The pitfall section below itemises which clauses to grep for before depositing.

Is +EV betting safer than arbitrage on offshore books?

Operationally yes, on the limit-survival axis. A +EV bettor places single sided bets that beat the closing market price; the bet pattern looks identical to a sharp recreational pattern and does not match the operator’s arbitrage detector. The trade off is variance: +EV has a real chance of losing money over a few hundred bets, while arbitrage locks the return inside the spread. The high stakes operation usually runs a hybrid: +EV as the primary engine for sustained edge, arbitrage on top of it for clearly large spreads where the void risk is worth taking, bonus arb on a separate account isolated from the +EV stack so a bonus void does not cascade.

Do tools like RebelBetting and OddsJam cover offshore books?

Coverage is partial and changes by quarter. The leading tools cover the largest offshore operator families that publish odds feeds reliably; they miss the Asian style books, most crypto first books, and many of the smaller operators where the arb edges are largest. The result is structural: tool surfaced arbs are by definition at operators that the tool-vendor has indexed, which means a meaningful fraction of arbing accounts are placing the same bet at the same operator simultaneously. The operators read the pattern as a tool footprint and apply void clauses or limit reductions accordingly. Manual scraping of the Asian style and crypto books is where the genuinely fresh arbs live, at the cost of operational overhead.

How do I bankroll arbitrage across many offshore accounts?

The operational rule is to keep enough float at every operator in the rotation to take both sides of a typical arb without rebalancing mid event. The float number is roughly two times the typical bet size at each operator, with at least three operators in the rotation. Rebalancing happens by withdrawing winning side balances after settlement and depositing into the losing side accounts, on a weekly cycle rather than an event by event cycle. The crypto cashier from the crypto offshore betting page is the rebalancing rail of choice because it settles the loop in hours rather than days; card and wire rails turn the rebalance into a multi day blocker that idles the bankroll.

What is bonus arbitrage and how does it differ from regular arb?

Bonus arbitrage is using a promotional credit (welcome bonus, reload bonus, free bet, risk free wager) to create a positive expected value bet, then hedging the live position at another operator to lock in the bonus value with reduced variance. The mechanics are spelled out on the bonuses page, but the headline is that a free bet is worth roughly seventy percent of its face value when hedged optimally on a single market, and a deposit match bonus is worth between forty and seventy percent depending on the rollover terms. The risk is that the same operators that publish the most aggressive bonuses are the operators with the most aggressive bonus abuse clauses; a positive bonus arb that gets voided is a negative outcome on every axis, including the deposit clawback the operator may pursue.

We use necessary cookies to make this site work. We would also like to set optional analytics cookies to understand how visitors use the site. You can change your choice at any time from the footer.